Should You Be Concerned About the Reintroduction of Adjustable-Rate Mortgages?

If you recall the 2008 housing meltdown, you may recall how popular adjustable-rate mortgages, (also known as an ARM). And, after years of being nearly nonexistent, ARMs are becoming increasingly popular when buying a home. Let’s look at why this is happening and why it’s not a cause for alarm.

Why Have ARMs Become More Popular Recently?

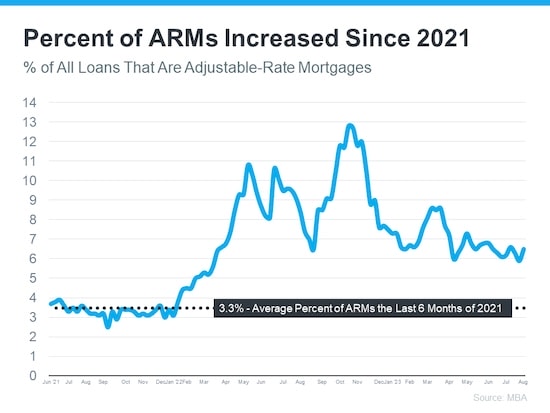

This graph uses Mortgage Bankers Association (MBA) data to demonstrate how the share of adjustable-rate mortgages has increased in recent years:

As shown in the data, after hovering around 3% of all mortgages in 2021, many more homeowners switched back to adjustable-rate mortgages last year. That growth has a straightforward reason. Mortgage rates increased considerably last year. With rising borrowing rates, several homeowners chose this sort of loan since standard borrowing prices were high, and an ARM provided them with a lower rate.

Why Are Today’s ARMs Not The Same As Those In ’08?

To put things into perspective, keep in mind that these aren’t the ARMs that were popular in the run-up to 2008. Loose lending rules contributed to the housing meltdown. When a buyer obtained an ARM, banks and lenders did not check verification of employment, assets, income, and so forth, people could get a loan without having to prove anything! Essentially, people were receiving loans that they should not have received. Many homeowners were put in jeopardy as a result of their inability to repay loans for which they were never required to qualify in the first place.

Lending requirements are different this time. Banks and lenders learned from the crash, and they now verify income, assets, employment, and other information. This implies that today’s buyers must qualify for their loans and demonstrate their ability to repay them.

CoreLogic Economist Archana Pradhan outlines the difference between then and now:

“Around 60% of Adjustable-Rate Mortgages (ARM) that were originated in 2007 were low- or no-documentation loans . . . Similarly, in 2005, 29% of ARM borrowers had credit scores below 640 . . . Currently, almost all conventional loans, including both ARMs and Fixed-Rate Mortgages, require full documentation, are amortized, and are made to borrowers with credit scores above 640.”

In plain terms, Laurie Goodman of the Urban Institute emphasizes this idea by saying:

“Today’s Adjustable-Rate Mortgages are no riskier than other mortgage products and their lower monthly payments could increase access to homeownership for more potential buyers.”

Summing It Up

If you’re concerned that today’s adjustable-rate mortgages will be similar to those used during the housing meltdown, rest assured that things are different this time. If you have questions about buying or selling a home in the Metro Atlanta area, we’d be more than happy to help! Just reach out to us at (404) 410-6465 or visit Complete Realty Team. We look forward to speaking with you!